I have a simple rule of thumb when it comes to news reports. The real story is always in the penultimate paragraph. Let's look at this inflammatory headline: Woman’s 'spree' after $158k banking error, refuses to return pensioner’s life savings An Auckland beneficiary is under investigation for an alleged “spending spree” after $158,000 was mistakenly transferred to her account. […] pensioner lo…

Continue reading →

Lots of people using banking apps on their Android phones. They're a convenient way to check your balance, transfer money to people, and get alerts about fraudulent transactions. But, like anything related to money, they can be abused. Nowadays, thieves are not only snatching phones, but forcing their owners to transfer money to the thieves. This is not an isolated incident. How can you…

Continue reading →

There's currently an open consultation about whether banks should have a lower compensation limit to refund their customers who have been scammed. Currently, if a customer falls for an Authorised Push Payment (APP) scam, they may be eligible for up to £415,000 back from their bank. The proposal is to limit this to a maximum of £85,000. What does this mean and is it a bad thing? APP fraud is w…

Continue reading →

There's an incredibly distressing story in the BBC about a vulnerable elderly man who was conned out of his life savings. Fraud victim gets surprise £153,000 refund despite rules BBC News In the story, the heartless bank refused to refund the fraud victim due to an absurd technicality - the money was sent to a foreign account rather than a UK account. Once again, big business bending the rules …

Continue reading →

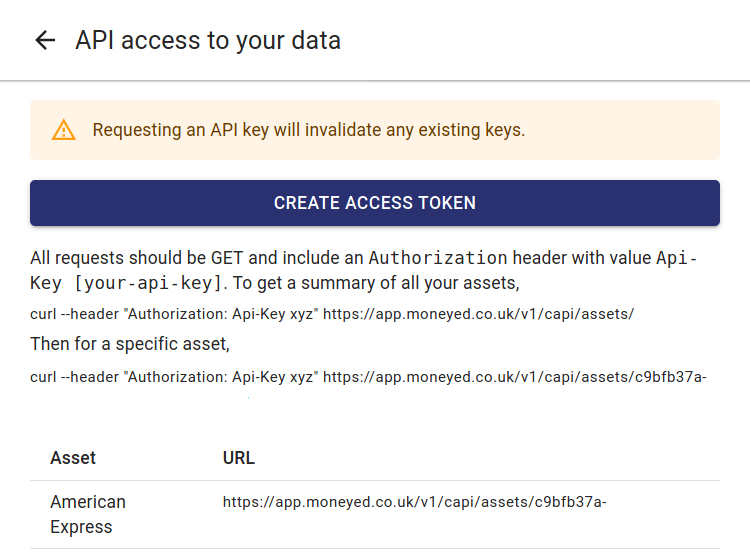

Update! Moneyed shut down in 2021. After writing about how to use MoneyDashboard's unofficial API, the good folk at Moneyed told me about their officially supported API! So here's a quick review & howto guide. Moneyed is a slightly strange service. I think it is designed for companies to give as a benefit to their employees. But you can sign up as an individual. The first month is free - but I…

Continue reading →

Note: MoneyDashboard is now closed. Yesterday, I wrote up how to use the MoneyDashboard Classic API. Read that blog post first before reading this one. MoneyDashboard have launched a new "Neon" service. The API is a bit more simple, but authentication is harder. Here's a quick guide to the bits of the API that I found useful. I've lightly redacted some of the API responses for my privacy. …

Continue reading →

Note: MoneyDashboard is now closed. The OpenBanking specification is brilliant. It allows you to aggregate all of your financial accounts in one place. You can give read or write access to apps and services. Magic! API access is restricted to registered financial institutions. That's good, because it puts up a barrier to entry preventing dodgy companies slurping up your data and sending all…

Continue reading →

I've blogged before about how backward the Co-op bank is - sadly, they've not improved in the last few years. I needed to close down my business bank account. I hopped on to online banking, provided all my details, went through 2FA with a physical token, remembered my mother's maiden name and began searching the site. There was no way to close the account. Oh well, I guess I'll give them a…

Continue reading →

When you create a QR code which contains a URL, it is vital that the code is not only as small as possible, but also as user friendly as possible. I'm not a massive fan of short URL services like bit.ly - but for shrinking the text you want to fit in a QR code, they are invaluable. I want to take a look at a particularly interesting example from Nat West Bank. The Poster Despite having the QR …

Continue reading →

It's Time To Switch Banks are fucking us over. They gamble with our money, lose it, ask us for a bail out, lose more money, then ask us for yet another bail out! They are resisting even the very modest changes the government is imposing on them. No more. We have a very easy way to stop the banks pissing about with our money. Take our money from them. I'm not talking about taking out your…

Continue reading →